Writeup #8 - Constellation Software: Mispriced or Broken?

After a 55% drawdown, is the VMS king broken, or is the market misreading AI?

Legal Disclaimer

The views expressed reflect my independent research and opinions and are provided for informational and educational purposes only. They do not constitute personalized investment advice, a recommendation, or a solicitation to buy, hold, or sell any security.

Nothing in this publication should be interpreted as a recommendation to take any specific investment action.

Whiteout Capital is a publication of Eudemonia 0x1 LLC, a Wyoming limited liability company. For full legal terms and disclosures, please visit whiteoutcapital.com/legal-disclaimer.

I own shares of Constellation Software (TSX: CSU) at the time of writing and may buy or sell shares of this company, or other companies mentioned, at any time without notice and may benefit from price movements in the securities discussed.

Constellation Software (TSX: CSU)

Stock price: C$2,471

Market cap: C$52b

A year ago, Constellation Software was one of the most widely regarded compounders in software.

Today, the stock is down >55% despite continued revenue and FCF growth.

The company now faces three headwinds—one operational, one strategic, and one market-driven.

Can the beaten up VMS king break through their headwinds and regain investor confidence?

Overview & History

Because Constellation is generally well-known, I’m going to skip a deep overview and assume readers have a basic understanding of their business. Instead, I’ll focus my energy on analyzing the current headwinds.

As a quick summary, Constellation Software is a 30-year-old holding company founded by former VC, Mark Leonard. They have historically wholly acquired vertical market software companies that are value-accretive and manage them as a decentralized web of subsidiaries.

If you have not heard of the business or would like to know more, here are a few high-quality resources I like:

Shareholder and annual letters: Mark Leonard, the founder, has written great letters going back many years. The best place to learn about the strategy is from the source.1

Business Breakdowns podcast: the Business Breakdowns hosts covered a few of the key strategic pillars of Constellation.2

Internal Constellation podcast: several years ago I came across this podcast episode that’s presumably an internal podcast made for Constellation employees.

Valuation Setup

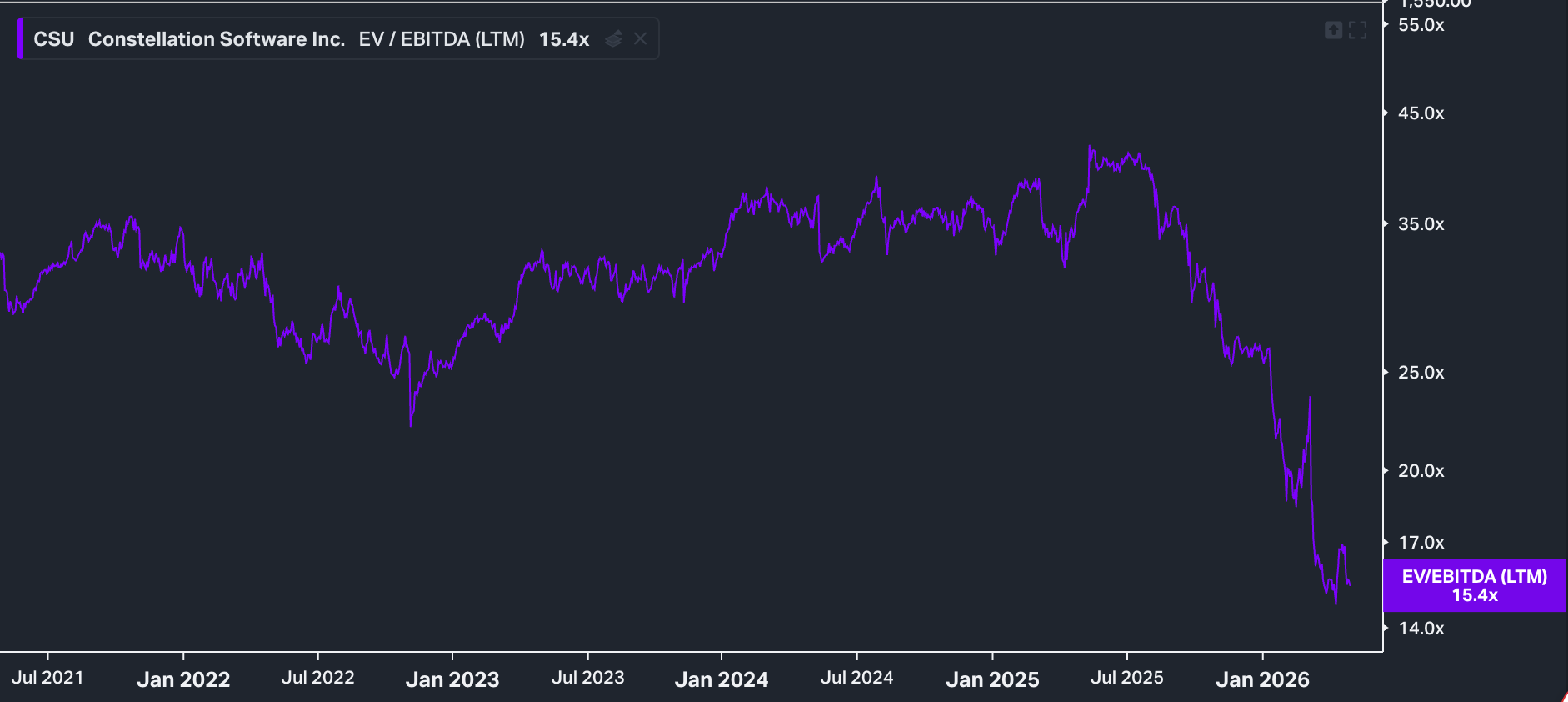

It’s impossible to say why a stock moves the way it does, but my interpretation of what happened to Constellation in 2025 is that the company went from being viewed as a faultless high-quality compounder to a company with serious risk and multi-layered uncertainty.

This led the EV/EBITDA to compress from ~40 on June 1st last summer to ~15 today.

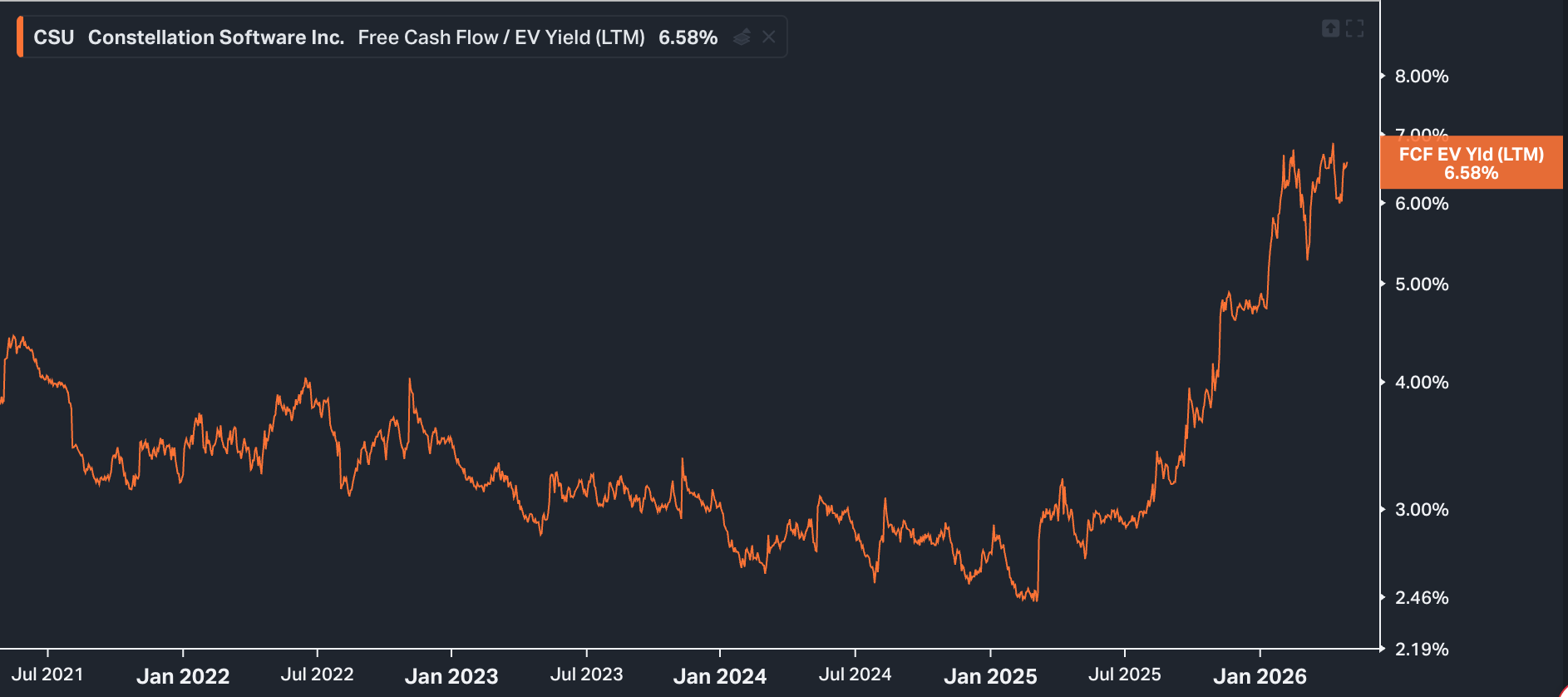

FCF/share was C$104.48 when they reported March 31, 2025 and was C$125.71 when they reported December 31, 2025, a 20.4% increase in three quarters. The combination of FCF growth and valuation compression has led the FCF EV yield to rise from <3% last summer to >6.5% today.

Looking at sales instead of FCF tells a similar story. EV/sales has approximately halved from ~7 last summer to ~3.5 today despite double-digit revenue growth over the same period.

The three horsemen headwinds

1. Mark Leonard stepping down

On September 25, 2025, Constellation announced that their founder and president, Mark Leonard, was stepping down from his role at the company due to “health reasons.”3 Mark is a very private person and there isn’t much to be found about him online despite the fact that he’s a billionaire, so we don’t know what he is dealing with or if we can expect him back.

Six months later, on March 27, 2026, Constellation announced that Mark will also be stepping down from the board, but will continue as an advisor of their Permanent Engaged Minority Shareholder (PEMS) strategy, which they describe as “an initiative centered on selective, long-term, and engaged minority investments that complement Constellation’s longstanding acquisition model.”4

Mark is often described as the “Warren Buffett of Software,” and Constellation is his brainchild. His leadership will be missed.

However, one of the core tenets of the company is their decentralized approach. Constellation isn’t one conglomerate of software products run by the head office, it’s a sprawling web of mostly independent subsidiaries that have taken the culture Mark established and implemented it at a much larger scale than any one person or head office could.

Constellation has spun out two holdings companies, Lumine and Topicus, and each of those companies has an umbrella of subsidiaries. Autonomy is granted to smaller teams and cash pay is based off performance metrics (share count is essentially unchanged since their 2006 IPO).

Constellation is a 30-year-old company with many long-serving employees. The culture and strategy are well-established and I think they have new people at the helm ready to guide the ship.

One of those people is Mark Miller, who took over Mark Leonard’s role as President and subsequently purchased C$4.99m worth of Constellation stock on December 12, 2025.5

We won’t understand the full downstream effects of this transition, possibly for several years, so this headwind is likely to stick around. My intuition says that given how decentralized the company already was, there may be a few hiccups, but things will generally keep humming along as they have for decades.

2. AI doomsday

I have read decent arguments that AI may broadly:

Reduce development costs, which will increase competition

Lower barriers to entry

Compress pricing over time

Accelerate feature parity

Commoditize software engineering

The combination of these factors has led many investors to assume that multiples of all software companies should contract and that the effects will be broad and deep.

While I think there is some merit to these concerns, not all software companies are created equal. Some, I would argue, are doomed to fail regardless, and while they may blame AI when that eventually happens, if AI hadn’t come around, the result likely would have been the same, but they would have blamed cheap foreign contractors, open source, etc. for their demise. The harsh reality is that for every software success, there are likely a thousand companies that failed despite motivated founders, financial backing, talented engineers, etc.

With that said, I do think some software companies will need to quickly change their business strategy…

Company FF example

A while back, our engineering team considered paying for a SaaS product that offers feature flag management. The core functionality of their product is to enable engineering teams to instantly turn features on/off, A/B test them, etc. Let’s call this company: Company FF.

The original tradeoff we considered was whether it was better to pay a monthly fee for feature flag control or if we should spend a few weeks homebrewing our own solution. We kicked the can down the road many times, developing a feature here and there as needed. We often reconsidered if we should just bite the bullet and upgrade to the paid service.

Then came Claude. We were recently able to implement all of Company FF’s features that we wish we had in a few hours.

To explain why I think this matters, I’ll introduce a simple framework that I’ve found useful when thinking about AI and software.